Who Will Own the Future of Regenerative Coffee? (pt. I)

The quest for new coffee genetics and the specter of corporate takeover.

I can’t remember what I originally set out to write about, but it quickly branched into several other themes, so I’ve split it into two parts. In this first section, we take a look at the state of the global coffee trade, current efforts to climate-proof the future of coffee production, and begin to talk about why all this matters to you.

Big Guns Enter the Regenerative Game

Recently, there have been some exciting announcements in the coffee sector regarding some heavyweight investments into regenerative farming. Sustainability has long been a buzzword in the coffee industry, but recently it seems that the term “regenerative” is popping up more and more.

Nestle and Starbucks have each revealed broader plans to incorporate more regenerative agriculture into their supply chains, and you don’t have to look hard to find similar language in other industry behemoths’ websites.

Of course, we’ll have to wait and see to what extent these pledges are upheld. Not only are the pledges largely self-enforced, but the companies themselves define their own success. After all, if Keurig Dr. Pepper (owner of Green Mountain Coffee) pledges to support regenerative agriculture on 250,000 acres of land, that sounds great until you realize that it only represents 50% of the company’s top “climate sensitive” crops. Nevertheless, it’s clear that some serious resources are being mustered around a level of ecological sustainability that may have been considered radical only a generation ago.

World Coffee Research: A Focus on Diversity

The coffee industry knows that climate change poses an existential threat, and one interesting example of the industry coming together to try to get out in front of the issue is World Coffee Research. WCR’s mission is to “ensure the future of coffee” through scientific research to improve the climate resilience of coffee.

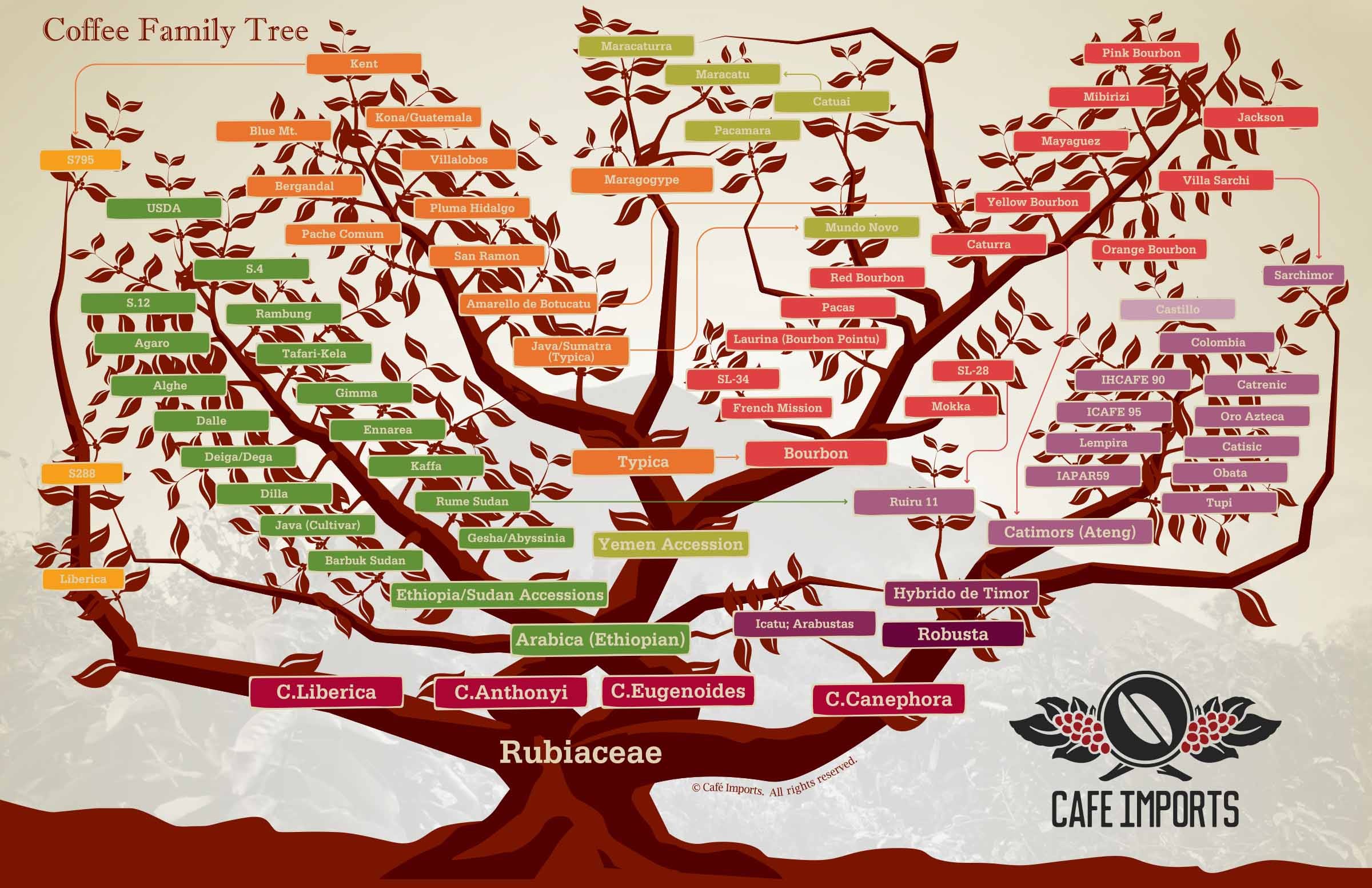

WCR’s flagship program is to research and develop new varietals of coffee that will be more resistant to the climate of the 21st century, and there is no doubt that this kind of work is long overdue. The vast majority of coffee varietals currently grown in the world are descendants of the Typica or Bourbon cultivars, which spread out of Africa and the Middle East via European colonial trade several hundred years ago.

Almost all of the world’s cultivated coffee is descended from the genetics of those original two plants, which means that there is a serious dearth of genetic diversity in the species Coffea arabica. Without the mutations that arise from genetic diversity, plants are vulnerable to diseases and pests and lack the hardiness to grow in adverse climactic conditions.

So, there’s no doubt that WCR’s work is urgent and necessary, and clearly, the coffee industry agrees. Just check out the list of WCR’s financial supporters— truly a who’s who of coffee titans, with household names like Folger’s alongside specialty pioneers such as Bluebottle and Intelligentsia.

Yet, here is where WCR’s stated mission to pursue genetic diversity clashes with the corporate realities of the global coffee sector today, which has been trending towards ever higher levels of consolidation for several decades now.

Consolidation Along the Coffee Chain

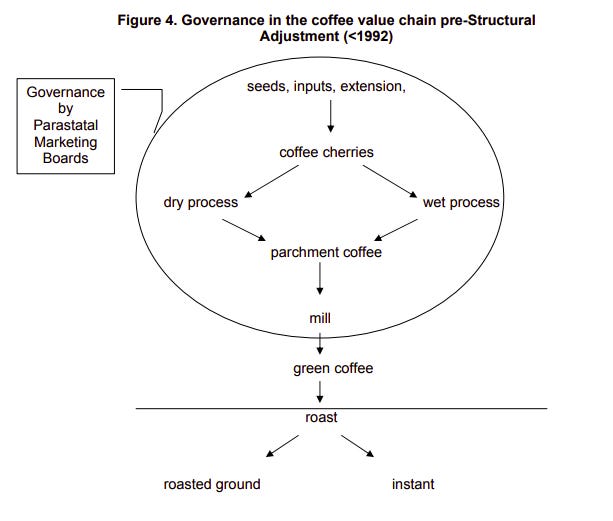

The coffee trade has a long and storied history, but for our purposes we can start in the post-World War II period. European countries were decolonizing and the United States was fully invested in containing communism. Thus, each northern bloc had their reasons for wanting to maintain stability and prosperity in the developing world. To this end, the International Coffee Organization was formed in 1963 to oversee the first International Coffee Agreement.

This agreement quickly evolved into a quota system whereby producing countries restrained coffee exports to maintain a balance of supply and demand, unless prices rose above a certain threshold, at which point the quota would be suspended, freeing producing countries to sell as much coffee as possible, which influx of supply would drive down prices.

The system was clunky but it basically succeeded in keeping coffee prices relatively stable for farmers for three decades until, in 1989, the system of quotas was suspended, and then, after years of failed negotiation, the scheme was officially abandoned.

With the Cold War winding down, promoting economic development in the Third World was less of a priority for the US. This was the era of “trade liberalization” and “structural adjustment,” and the quota system that regulated the coffee trade didn’t mesh with the U.S.’s philosophy on Free Trade at the time.

The abandonment of the ICA had a disastrous effect on coffee prices, which quickly bottomed out to levels never seen during the ICA period. In Brazil, where coffee is often planted in full-sun rows after native forests are razed, coffee production was ramped up to take advantage of its economies of scale. Vietnam also increased coffee production drastically, setting the stage for a chronic oversupply problem in the coming decades.

The Global Coffee Supply Chain Reshuffle

During the era of the ICA, the coffee sector was already quite concentrated, with five firms splitting the majority of the world’s imports. Today, that number is even more concentrated, with three firms controlling the majority of the world’s imports: Neumann Kaffee Gruppe, Volcafe, and ECOM.

In the post-ICA era, these massive firms took the opportunity to vertically integrate their supply chains, snapping up farms and export houses in producing countries the world over. Let’s look at Neumann Kaffee Gruppe as an example: besides outright owning several farms around the world, EKG manages mills in almost every major producing country in Latina America and Africa. They also are the parent company to well-known specialty importers InterAmerican and Atlas Coffee.

Essentially, the previous model of large firms from consuming countries negotiating with the national coffee boards of producing countries was replaced with international firms working directly in producing countries.

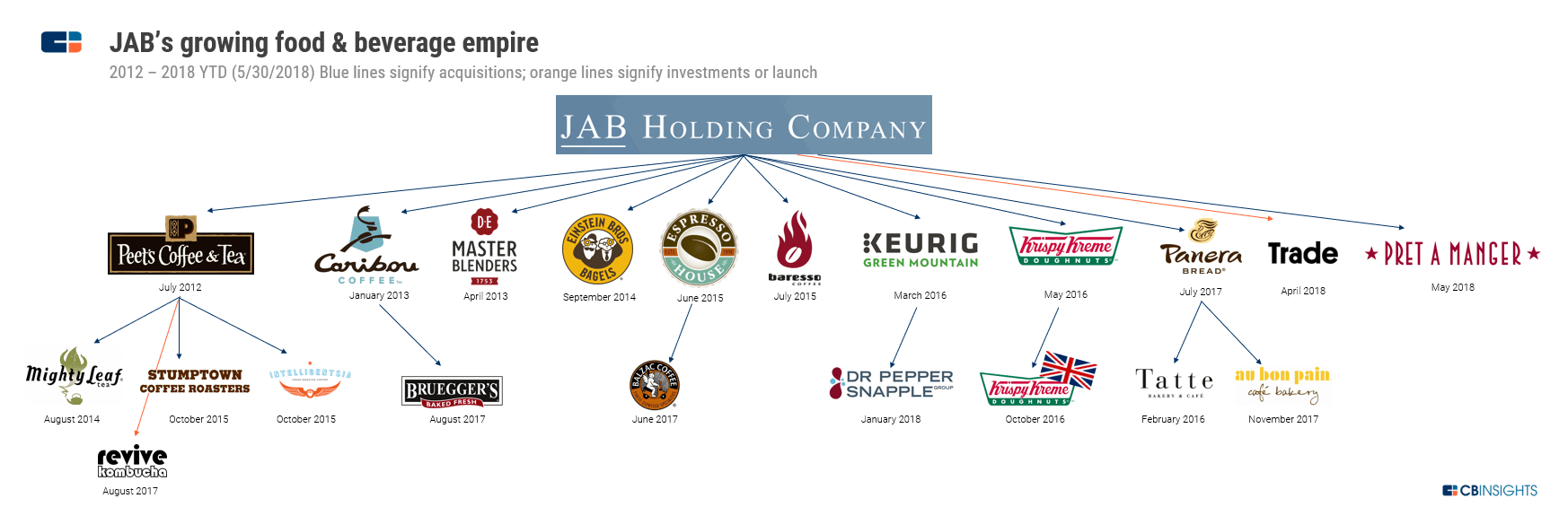

Consolidation has also been a hot trend among the consuming side of the coffee equation, and the scale of these mergers and acquisitions is really quite impressive. After all, we all know Dunkin Donuts moves an enormous amount of coffee, yet they are only one brand in the JM Smucker’s/ Folger’s portfolio.

Capsule-coffee drinkers may be surprised to find that the Keurig, Green Mountain, and Donut Shop Coffee brand pods are all actually owned by Keurig Dr. Pepper (along with Midwest chain Caribou Coffee).

Yet Keurig Dr. Pepper is actually itself a holding in the portfolio of JAB Holdings, a privately-held group whose other investment in the coffee and tea space is JDE Peet’s, which owns west coast pioneer Peet’s and over a dozen other brands, including specialty powerhouses Intelligentsia and Stumptown.

{kind=link}

{kind=link}

Bluebottle, another specialty roaster with near-household recognition, is itself owned by Nestle, which, besides its own omnipresent Nescafe brand, also owns Starbucks’ distribution.

The upshot of all these vertical integrations, mergers, acquisitions, distribution deals, brand portfolios, etc. is this: behind the appearance of diversity of choices for coffee is an extremely narrow concentration of capital into a few companies which leverage a high degree of control over the product from the farm level all the way to the cup.

Keep a lookout for the second half of this exploration into the state of the global coffee trade and who is doing what about climate change within it.

nice, I read this post. as a 10 year experience in this field i wiil suggest you're considering a Sample Coffee Roaster and Coffee Bean Drum Mixer, explore your options on our website, Coffee Pro Direct!

http://coffeeprodirect.com/

https://coffeeprodirect.com/coffee-sample-roaster/