A Looming Coffee Crisis

A Looming Coffee Crisis

Our Five-Year Outlook on the world of coffee

Zach, one of the cadets, is returning from a trip to Guatemala where we met with our Antigua-based farmer partner Manuel to get an update on the 2024 harvest. We also attended a two-day forum where we were able to connect with farmers, traders, and roasters from from all over Central America. Overall there was a mix of deep concern and cautious optimism about the state of coffee production globally, which we will summarize below.

CONCERNS FOR 2024 AND BEYOND

I am not one to be overly dramatic when talking about the coffee industry. True, I’ve worked side-by-side with farmers struggling in the most impoverished conditions imaginable. I’ve come face-to-face with the deeply human effects of the inequality inherent in the global coffee trade. These experiences have shaped my approach to coffee in that my passion is first and foremost always for the wellbeing of the small farmers who are the backbone of this industry. However, rather than engage in emotional arguments, I always am looking to better understand the emotionless logic– the market logic, so to speak– that is the invisible structure of this industry.

All that is to say that what I am about to write is not an appeal to emotion, nor based on an emotional response to the current state of the industry. I certainly am concerned, but that concern is based on the fact that now, more than ever, several economic factors are lining up that provide a deep cause for alarm for all of us who care about the people in the coffee supply chain or just value a good cup of coffee. These economic factors can be summarized as: a profitability crisis at the farm level and climate change’s havoc-wreaking effects.

WHY CAN’T FARMERS SEEM TO GET AHEAD?

Coffee farmers are not feeling optimistic about the future, and that’s a problem. If they can’t make a living growing coffee, they will turn to other crops or leave farming altogether. Less global supply means less great coffee to choose from, and higher prices for all of us.

What is currently squeezing farmers’ profitability? In my recent trip to Guatemala, over and over again I heard the same thing: immigration.

Guatemala’s Labor Drain

Those of us in the US are used to hearing about waves of migrants coming to the US across the southern border. For me, it’s been hard to decipher how much of the media attention on immigration is real or manufactured. But in Guatemala and the other Central American coffee countries, the effects are real, and concerning.

One agricultural technician who works on USAID projects to increase farmer productivity told me that he started a new project with a group of 100 farmers. By the time the program ended, 40 farmers had left. A 40% attrition rate is alarming.

Many farmers expressed not being able to find workers to pick coffee during this harvest. Working as a coffee picker is hard work to say the very least, so it’s no wonder that many of those who struggle to survive in this unforgiving line of work would prefer to try their luck at a new life in the US. However, there is an outsized effect of this immigration back in their home country: once their relatives start to receive remittances from their emigrated relatives, they prefer “not to work,” as their compatriots claim, although I suspect many just prefer to do anything but work as lowly-paid coffee pickers.

The lower supply of labor has resulted in higher wages for the workers who remain, but there is a limit to how much farmers can raise wages. A woman I spoke to in the Antigua area told me that the current price for coffee for one quintal (100 lbs) of coffee cherries is currently 200 Quetzales– about $26 USD. But the prevailing wage to coffee pickers is currently 60 Quetzales per quintal. So farmers are taking 30% right off the top before taking account of input costs– which have doubled or tripled since the start of the Ukraine conflict– or any other expenses, leaving very little room to make any profit.

It’s worth noting that coffee production outside of Brazil– where coffee is planted in flat-lying areas, allowing a high degree of mechanization– is heavily dependent on labor. Countries like Guatemala have earned a reputation for high-quality coffee (and the premiums that go with it) largely because the coffee is hand-picked, selecting only the ripest cherries at harvest. With the labor pool drying up, farmers have to make tough decisions about how to get the cherry off the tree and into the market– possibly by either being less selective or by leaving cherries to dry on the branch.

Lower Margins Are Leading to Reduced Reinvestment

The labor shortage combined with the aforementioned steep rise in fertilizer costs has a further compounding effect: reduced fertilizer usage. When the Ukraine conflict first disrupted fertilizer costs, many farmers simply couldn’t afford to apply fertilizer at adequate rates and so lowered their input usage. With coffee being an annual crop, the effects on yields has taken some time to play out, but we are seeing now several years in a row of lower harvests.

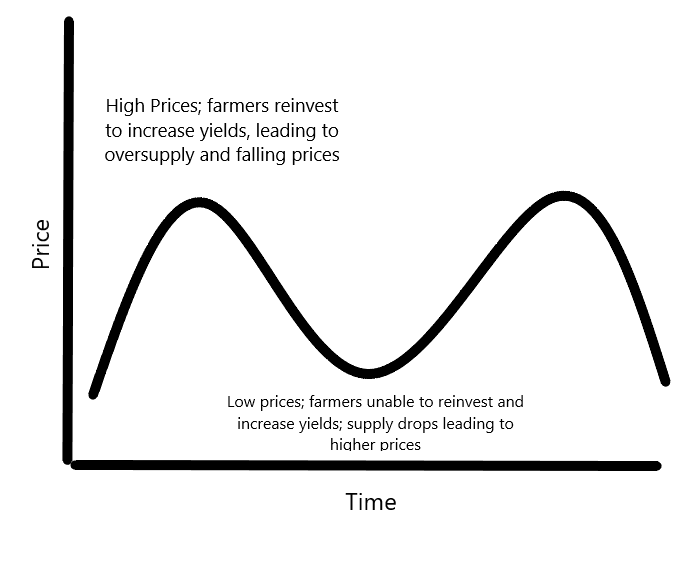

Theoretically, less supply of coffee should lead to higher prices, but it can take time for those higher prices to play out, and in the short term, farmers see reduced income, leading to more challenges hiring labor and buying inputs, which further compounds the problem.

Overall, I still see fundamental market forces at play here: all of these compounding issues must inevitably lower the supply of available coffee, which in turn will drive up the price. With higher prices, farmers will again be able to make the economics of their farms work, investing in their land, improving quality and productivity until supply rebounds, which will eventually start to put downward pressure on prices, at which point the whole cycle will begin to repeat itself in a classic agricultural economic pattern.

The question, then, is where are we in the coffee price cycle? Curiously, people who regularly buy coffee from farmers might not be of the same opinion that prices are lower than ever. Indeed, C-market prices have remained above $1.50 and indeed closer to $2.00/lb for the last year, and, except for a brief but spirited dip into the $1.40’s in the Spring of 2023, have traded just north and south of $2.00/lb since around 2020. For reference, during the more recent coffee “price crisis” in the mid 2010’s the C-Market price was dropping below $1.00/lb.

So from the prevailing pessimism of $1.00/lb the market has been sticky at around double that price. Shouldn’t the narrative be that prices are rising (as would be expected) and therefore see rising investment in farms, increased productivity, and a positive outlook– in other words, we are on the upward trend of the price cycle?

In fact, the rapid inflation of 2020 and onward appears to be obscuring the fact that actual income to farmers has not really gone up. If we adjust for inflation, the price of coffee for farmers has not really gone up all that much, if at all, from those previous crisis levels. If that is the case, we are probably still approaching the (inflation-adjusted) bottom of the price cycle, and can expect prices to increase in the coming years.

Indeed, this is my outlook. I can’t see how prices can go lower over the next few years considering the conditions I detailed above. There is no way any form of mechanization can relieve the labor shortage in Central America in the short term.

For buyers of coffee (traders and roasters) this is particularly worrisome, because many businesses have struggled to make the economics work with the C-Market around $2.00/lb. What would happen if $2.00 is the new “price crisis” level and $3.00 is the new “normal?” After all, the C-Market is just a reference for specialty coffee brands, with most paying a further premium on top of that price anywhere in the range of $0.50-$2.00 or more. Coffee companies all took price increases over the past few years, so consumers might not be prepared to stomach further increases in the coming years.

Scary stuff, and we haven’t even talked about climate change yet!

THE CLIMATE PROBLEM

The reality of a changing climate is another fact on which all the farmers I spoke with agreed. If the labor and profitability crisis is at the forefront of farmers’ minds, the climate issue is the dark specter looming over everything in a much more ominous way.

Fundamentally, the weather is getting more volatile. Dry spells are getting longer and dryer. It’s been hotter as well– noticeably hotter this year than any year in the past five years I’ve been coming to Guatemala. Rainy periods are more infrequent and come at unexpected times.

In Antigua, where we have the most experience, this is particularly concerning. The volcanic soils on the slopes of Volcán de Agua where our farmer partner, Manuel, works, are sandy and drain water quickly. In this tropical country, where seasons alternate between rainy and dry, and at this high altitude, where humidity is inherently low, this means that the “summer” or dry season is starting to resemble more desert-like conditions for long stretches of time. And if the rains come late or leave early, we are looking at period of five or six months with basically no precipitation, leaving no water in the top several inches of the soil.

Another side-effect of higher temperatures is that when the rain and humidity does come, it provides a perfect breeding ground for fungal diseases like coffee leaf rust (la roya) which can devastate coffee plantations. For farmers at super high altitudes like Manuel, la roya was never a concern previously, because temperatures naturally stayed cooler where his plots are. Now, however, incidences of roya are increasing. Perversely, long periods of drought take the edge off of this threat, but in more humid areas where rainfall is not a problem, roya and other fungal diseases are now becoming constant and pervasive.

These climate issues are bringing a new level of unpredictability to coffee farming which further complicates the labor and profitability issues detailed above. At a certain point, I have to wonder how far away we are from a large-scale crop failure scenario. I don’t think we are quite there yet, but the possibility over the next few years is certainly increasing. In any case, the “Valley of the Eternal Spring” where Antigua is located is certainly starting to feel a lot more like the Valley of the Eternal Summer.

TAILWINDS, OPPORTUNITIES, POSITIVE NOTES

It’s not all doom and gloom in the coffee lands. I’m a firm believer that crisis breeds opportunity, and the opportunities that are a response to the multiple acute and looming crises are beginning to shape themselves.

First of all– and I may be biased– but the buzzword at the Producer-Roaster Forum was definitely “regenerative.” It’s amazing to think that just a few short years ago, when we first conceived of Biota Coffee, the phrase “regenerative agriculture” was barely known. Indeed, I used to describe what we were trying to do as “beyond organic,” which illustrates how there wasn’t even really an accepted term to describe what we were trying to do, which was to go beyond just not using chemical inputs and actually restore soil health and biodiversity.

Now, however, a real movement is starting to coalesce around this concept of regeneration, and it’s easy to see why: conventional agriculture is generally monoculture and dependent on heavy fertilizer, herbicide, and pesticide use. It recommends the removal of shade trees in order to boost yields in the short term (more sunlight = more photosynthesis and increased plant metabolism) but leaves the plant exposed to harsh heat and drought conditions. Conventional agriculture is primarily focused on yields. Farm yields X market price = Income.

Regenerative agriculture, on the other hand, stresses profitability. It reduces external inputs by increasing circularity at the farm level, where all organic materials are recycled as compost, a fertilizer of superior quality over chemical pellets. It encourages the natural immune system of coffee plants to defend against pest and disease, and reduces the extremes of climate via diverse shade canopies which stabilize temperature extremes.

Furthermore, regenerative agriculture encourages diverse income streams by planting a variety of edible or commercial crops. On Manuel’s plots, for example, I was able to count lime, avocado, yucca, pineapple, banana, plantain, and jocote (a tasty and tart fruit) trees, on top of the non-edible nitrogen fixing species such as Inga. All combined, these different crops can help provide multiple sources of year-round revenue, not to mention continuous tasty and healthy food for the farmer and his family.

Another positive note is that all of these plants get pruned directly onto the ground. In the long term, they will compost into the soil, providing a slow drip of nutrients to the coffee plants. In the short term, however, they also cover the soil and reduce evaporation, helping to hold water as long as possible. This benefit is becoming increasingly critical.

We are also super pumped about Manuel’s new raised drying beds which he is using to dry the coffee this year. These beds are basically just mesh screens in a wooden frame, but their impact on coffee quality is huge. As opposed to drying on a concrete patio, air can pass underneath and through the cherries in a raised bed, which contributes to a much more even drying. More even drying allows more even roasting, which produces a superior cup. We can’t wait to taste the new coffees coming in from Manuel this year and have high hopes they will exceed last year’s crop, which frankly has been tasting pretty stellar so far.

Lastly, although the past few years have been somewhat modest harvests for Manuel, already there are huge clusters of buds sprouting on the coffee plants. These buds will produce flowers which, after pollination, become coffee cherries. Thus, the buds are an early indication of next year’s harvest, and so far, it looks like 2025 will be a monster year.

So, if you haven’t already recommended Biota to friends, family members, and colleagues, now is the time, because we will have plenty of coffee to sell down the road! In fact, why don’t you pass them my personal code (ZACHARYLATIMORE-JRC-QMF) so that they can take a discount off their first order– or you get your own code after your first purchase of Biota and keep the affiliate rewards for yourself.